Close Advanced Search Filters

Search

Topics

Content Types

Results > Audit and Assurance: (16)

Advanced Search Filters

Clear Filters

Summary

Wednesday, May 15, 2024

AAA Impact Hub

Examining the Role of Falsified Accounting Reports in Ponzi Schemes

Researchers investigate the role of accounting in Ponzi schemes, specifically focusing on how the provision of accounting reports, such as falsified financial statements and fictional audit opinions, affects investors' trust and the...

Summary

Wednesday, May 1, 2024

AAA Impact Hub

How Do Cybersecurity Breaches Influence IT Governance Roles in Audit Committee Charters?

The researchers investigate why certain firms tend to incorporate Information Technology Governance (ITG) roles into their audit committee charters and identify the factors influencing this process.

Infographic

Tuesday, April 30, 2024

AAA Impact Hub

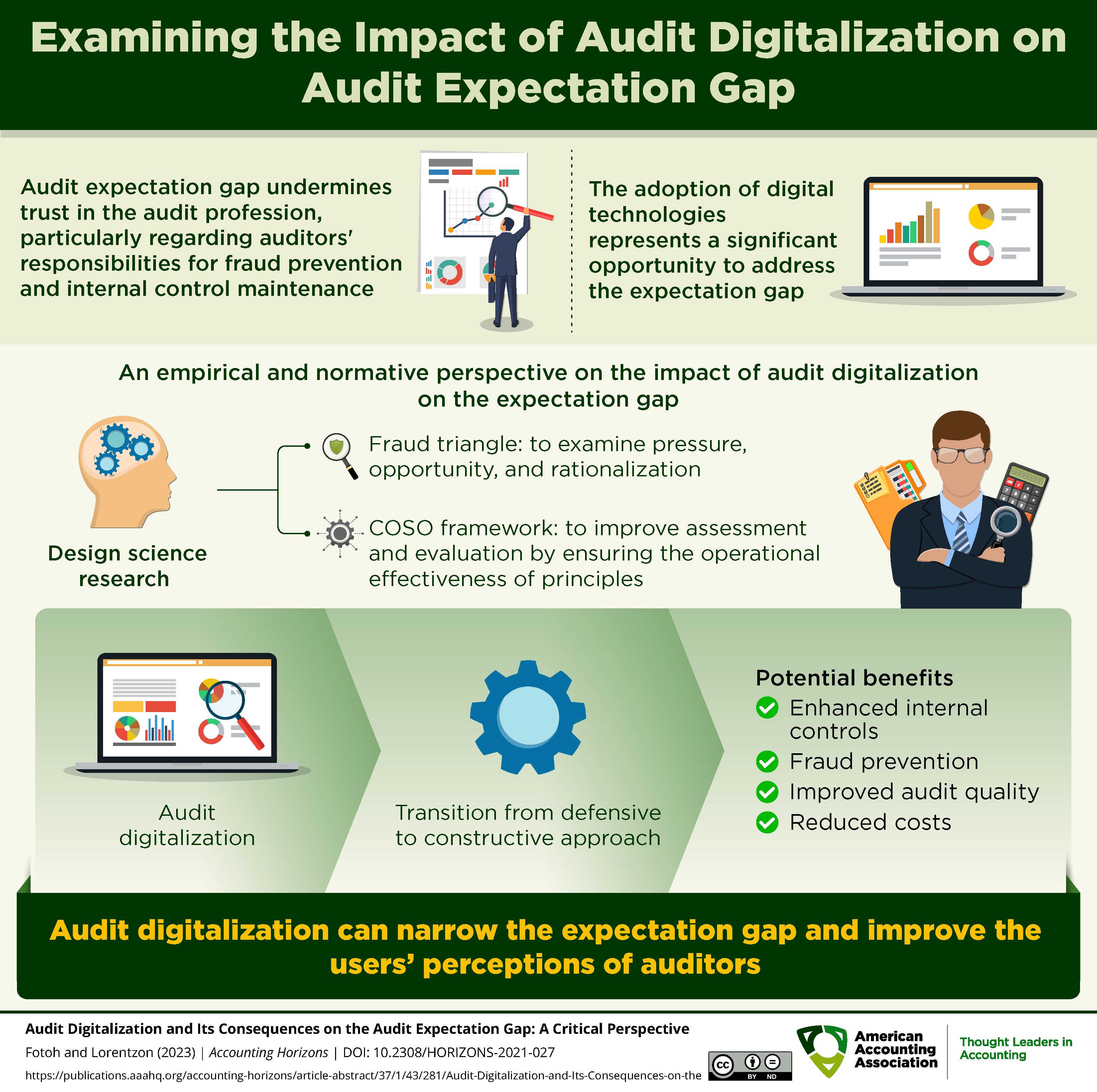

Examining the Impact of Audit Digitalization on Audit Expectation Gap

The audit expectation gap—broadly defined as the difference between how those who use financial statements view the role of auditors versus the beliefs of the auditors themselves—has caused friction for decades. This study delves into...

Summary

Tuesday, April 30, 2024

AAA Impact Hub

Audit Digitalization: Narrowing the Expectation Gap

The audit expectation gap—broadly defined as the difference between how those who use financial statements view the role of auditors versus the beliefs of the auditors themselves—has caused friction for decades. This study delves into...

Summary

Tuesday, April 30, 2024

AAA Impact Hub

Does Team Diversity Within Audit Offices Impact Audit Quality?

The researchers look at whether having diverse audit teams in accounting firms, especially those within the Big 4, affects the quality of their audit work. The study explores if teams that include people from various backgrounds...

Summary

Tuesday, April 30, 2024

AAA Impact Hub

The Role of Public and Private Enforcement in Measuring Accounting Irregularities

This study addresses the intersection of public and private enforcement in detecting accounting fraud and irregularities, contrasting the effectiveness and outcomes of actions taken by the Securities and Exchange Commission (SEC) and...

Summary

Tuesday, April 30, 2024

AAA Impact Hub

Examining the Effects of Auditor-Provided Tax Planning and Compliance on Tax Outcomes

This study explores the relationships between auditor-provided tax compliance and tax planning services and their impact on corporate tax avoidance and tax risk. The researchers investigate how engaging auditors for tax services influences...

Summary

Thursday, April 25, 2024

AAA Impact Hub

Does Audit Practitioner Feedback Influence PCAOB Auditing Standards Development?

This study focuses on how feedback from audit practitioners influences the development of auditing standards by the Public Company Accounting Oversight Board (PCAOB), which oversees auditing practices...

Summary

Tuesday, April 16, 2024

AAA Impact Hub

Examining the Impact of Auditor Diversity on Financial Examination Quality

This study examines how the characteristics of auditors signing an audit report influence the quality of financial examinations for listed firms in China.

Summary

Tuesday, April 16, 2024

AAA Impact Hub

How Do Auditors Assess Managerial Competence Following Internal Control Failures?

The study examines how auditors assess managerial competence following an internal control failure, investigates “omission bias” in assessments, and suggests ways to lessen its impact.

Summary

Tuesday, April 16, 2024

AAA Impact Hub

How Do Employee Satisfaction and Work-Life Balance Affect Audit Quality in Accounting Firms?

The study investigates how employee satisfaction and work-life balance within accounting firms are related to the quality of their audit services.

Summary

Tuesday, April 16, 2024

AAA Impact Hub

Is Big 4 Experience Linked to Higher Audit Quality?

The study investigates whether non-Big 4 audit firm partners with Big 4 experience command higher audit fees and if this experience translates into higher audit quality.Powered by Lead Marvels, Inc 2024